Let’s be honest. Budgeting is hard. Starting a budget is hard. Maintaining it is even harder. When I worked endless overtime, I completely gave up on my budget. There was no need. After all, I was saving, investing, and spending at my leisure, and always had enough money in the bank. What was the point? As someone who budgeted for years before that, I should have known better.

Our world has changed, and with it, our budgets. I can’t operate on the same budget I did when I was 20 years old, and I shouldn’t expect to. Between my full-time job, part time job, and overtime, I am making about $90,000 pre-tax.

As a single woman with a mortgage and varied expenses, sometimes I feel the stretch. At the same time, I like to have fun. I love to travel and go to sports events. I have a blast going to concerts, and enjoy the occasional dinner out. So how do I manage to do these things in today’s economy? A budget.

Why Budgets Are Important

I get it. Budgeting sounds so…restrictive. But it doesn’t have to be! It just needs to fit your lifestyle. At the same time, you need to be willing and able to make some sacrifices. In the words of finance influencer, Paula Pant, “You can afford anything, but not everything.” Unless you make a significant amount of money, you likely can’t max out your investments, save for a house, save for a car, and take ten vacations a year. You have to prioritize what financial goals are the most important to you and plan your budget around those.

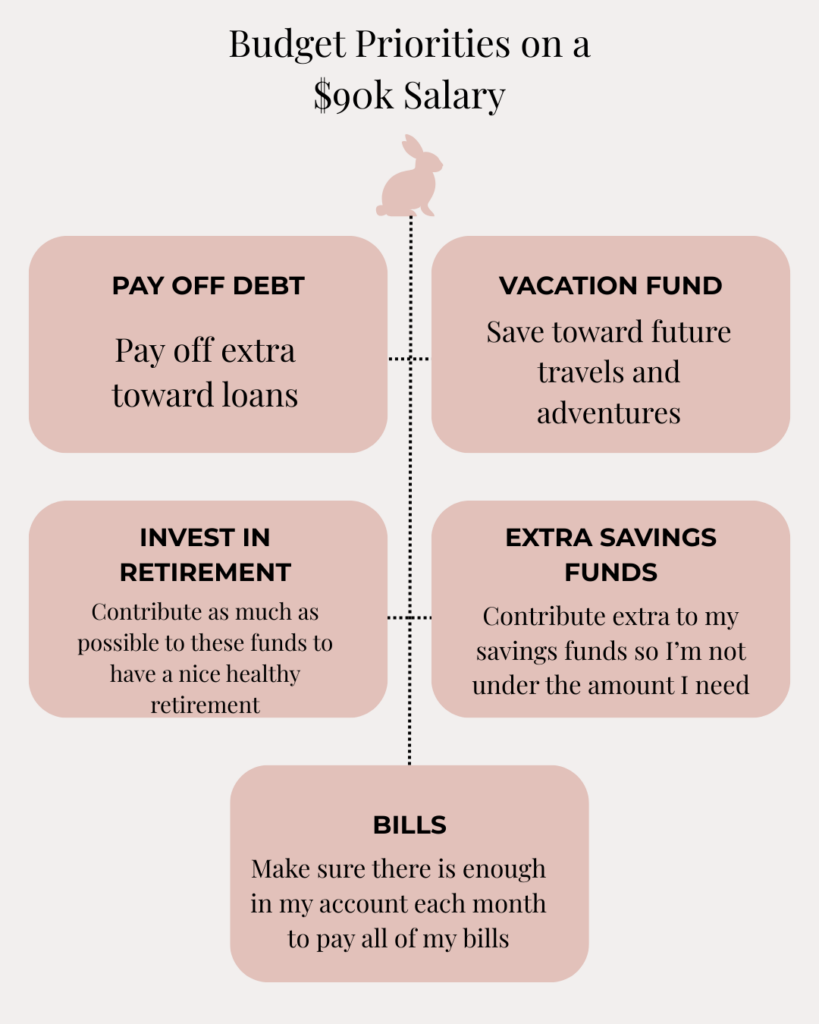

Here are my main budget priorities:

- Pay off debt – I have two loans. I am making the required monthly payments on them and have allocated an extra portion each month to contribute toward paying them off faster.

- Vacation fund – travel is important to me. It helps me escape and get away, and I just love seeing new places and visiting old friends.

- Invest – every check I have a set amount of my income withdrawn automatically into my retirement accounts. It is extremely important to the future I want to have these accounts keep growing.

- Bills – I have never felt the pressure of having an upcoming bill and not having the money in my account to pay it, and from the stories I hear from others, I don’t want to.

- Extra savings – I have plenty of other savings funds that help with my financial goals. Some examples include: an emergency fund, a sinking fund (a savings account where you save for a future expense each time you get paid) for my car insurance, and a future car fund

Budgets are important because they help you break down and prioritize these goals. By allocating set amounts from my check each month to these budget categories, I’m helping my goals grow without much thought or worry.

How to Prioritize Budget Categories Based on Your Income

If you don’t already know what goals you want to prioritize, or even what your goals are at all, I recommend you pause now and write some down. If you don’t currently have any goals, I recommend you start with the basics. Make sure you have an emergency fund and some healthy savings, and then invest the rest.

So how do you build a budget that allows you to enjoy life while still paying for all of your necessities? I hate to break it to you, but there’s no way around it. You’re going to have to do some math.

It can be time consuming to dig into your finances and truly find out how much you are spending and bringing in, but there is really no way to do a budget without knowing these numbers. You need real numbers, not guestimates. I promise, you will either forget something, or you will be wrong.

Once you know the nitty gritty of what you’re bringing in and what is coming out, you will also know if you have (or should have) money left over each month.

And this is where the prioritization comes in. Maybe one spending category is a little higher than it needs to be. You can allocate some of that income to another goal. Or maybe you have a few hundred dollars extra each month. I would contribute it toward whatever your top goal is.

What to Do If Your Numbers Aren’t Adding Up

So what do you do if you’ve done the hard work and the numbers just don’t add up. You have your income and expenses, and at the end, you are spending more than your saving. You can’t budget for your priorities because there is no extra money lying around.

It’s time for some tough love. There is a VERY good chance that if this is you, you may not be making enough to get by. In cases like this, there is really only one option. You need to make more income. Sure, you can look at other options first. Maybe downsize your apartment, or sell your car off for a cheaper one. But as anyone who has tried it knows, that’s no where near as easy as it sounds, and sometimes is impossible. That leaves only one thing. Increase your income. Here are some helpful ways you can do that, if you want to reach your own financial goals and not feel deprived.

- Take on a second job – I can tout my financial prowess all I want, but one of the biggest reasons I have a lot of the things I have isn’t because I’m the world’s best budgeter. It’s because I have a second, part-time job, and I’ve held it for years. This has helped me pay off loans, buy season tickets for my favorite sports team, and enjoy life without struggling. If you have the time and means and it would be difficult to leave your job right now, I highly recommend this

- Get a higher paying job – I know this one isn’t as easy for everyone, but I promise, it is an option. Maybe you feel stuck, or like you don’t have the skills to get a better paying job. I recommend checking out your local library or community resource centers. They can help with certifications, training, or finding resources you can use that would help you learn the skills you need to get a better paying job.

- Ask for a raise – this one can be daunting especially if you have one of “those” bosses. However, if you are in a good place with your employer, are doing well at your job, receive good feedback, and/or noticed you might be making less than your job and experience says you should, TAKE THE RISK. I have heard countless stories from those who were scared but asked for a raise anyways, and got it! Just be prepared. Stay calm, show your worth, present your case, and ask. The worst they can do is say no, but if they say yes, you just got more income!

If you plan on using any of these methods to raise your income, a good question to ask yourself is, what would my ideal budget look like. If I wanted to save $1000 a year for a vacation, how much extra income would I need to make that happen? This helps give you a starting point for both your budget, and might help you determine what jobs you are willing to look for and take based on your goals.

How to Budget Without Feeling Deprived

The truth is, the best way to budget without feeling deprived is to make enough to be comfortable, pick your HIGHEST priorities, and save for those.

Step one is to make sure you are living within the means of your salary. Making $90,000 gives me a comfortable income that pays for my monthly bills and expenses and still have money left over for my goals.

Step two is to pick the priorities that are most important to you. I have a lot of goals, but if I tried to save for 15 things at once, I’d be contributing very little toward each one. By having just two or three high priority goals, I can focus on those, watch them grow, and reach them sooner.

Step three is to reevaluate frequently. I check my finances every month, and I recommend you do too. This helps you stay on track, remember your goals, and focus on what’s most important to you…financially. Honestly, anything longer than a month is a big no for me. Two months can easily turn into three, then four, and before you know it, you no longer check your budget or your priorities. If you have the time, I recommend doing a basic check in once a week, even if it’s five minutes, and then a longer check in monthly.

I’m sure some of the things here aren’t what you wanted to hear, but the truth is, there is no magic system that finds money for you out of no where. The best thing you can do for your financial picture is to make enough income to cover expenses, prioritize your financial goals, and pick the top ones.